How realistic is a North American currency?

Commentary: Uniting U.S., Canada, Mexico money could result from crisis

By Todd Harrison

Last update: 6:12 a.m. EST Jan. 28, 2009

"World, hold on. Instead of messing with our future, open up inside." -- Bob Sinclair

NEW YORK (MarketWatch) -- Thomas Jefferson once said: "When you reach the end of your rope, tie a knot in it and hang on." As the global financial system pushes on a string, investors are desperately trying to hold tight.

The New World Order is upon us, full of hope, promise and a fair amount of fear. In our recent discussion regarding the direction of our country, we noted the risks of catering to conventional wisdom and the implications for the U.S. dollar.See MarketWatch column on New World Order.

The Minyanville mantra is to provide financial news you need to know before you know you need it. That's a fine line to walk, as foresight often flies in the face of mainstream acceptance.

In 2006, it seemed counterintuitive to forecast a "prolonged socioeconomic malaise entirely more depressing than a recession." See Minyanville column.

For years, the notion of an "invisible hand" was conspiracy theory until we learned that the Working Group on Financial Markets was a central policy tool. See Minyanville column.

And now, as we gaze across our historically significant horizon, we must open our minds to thoughts and ideas that may seem foreign to folks conditioned by the past and stunned by the present.

Currency crossroads

As governments take on more risk -- as they price assets on behalf of the market and transfer debt from private to public -- the common denominator, or release valve, becomes the currency.

If our economic condition is allowed to take medicine in the form of debt destruction, the greenback will appreciate, and asset classes as a whole will deflate. If we continue to inject drugs that mask symptoms rather than address the disease, the likelihood of a seismic readjustment increases in kind.

As governments take on more risk -- as they price assets on behalf of the market and transfer debt from private to public -- the common denominator, or release valve, becomes the currency.

If our economic condition is allowed to take medicine in the form of debt destruction, the greenback will appreciate, and asset classes as a whole will deflate. If we continue to inject drugs that mask symptoms rather than address the disease, the likelihood of a seismic readjustment increases in kind.

The deflationary forces in the marketplace are pervasive, and the "other side" of our current equation, hyperinflation, may be years away. Given the magnitude, breadth and pace of the global financial epidemic, however, we must explore each side of the twisted ride.

Years ago, the Federal Reserve wrote a "solution paper" regarding the need to combat zero-bound interest rates. The concern was the flight of capital from the U.S. and an option discussed was a two-tiered currency, one for U.S citizens and one for foreigners.

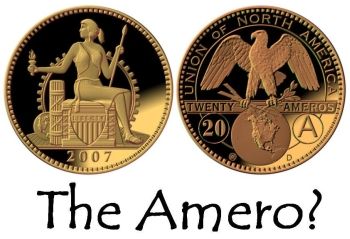

Canadian economist Herbert Grubel first introduced a potential manifestation of this concept in 1999. The North American Currency -- called the "Amero" in select circles -- would effectively comingle the Canadian dollar, U.S. dollar and Mexican peso.

On its face, while difficult to imagine, it makes intuitive sense. The ability to combine Canadian natural resources, American ingenuity and cheap Mexican labor would allow North America to compete better on a global stage.

Experience has taught us, however, that perceived solutions introduced by policy makers and politicians don't always have the desired effect.

Unintended consequences

I've long contended that, much like the Internet prophecy proved true -- but not before the tech crash -- so too would globalization, albeit not without painful-yet-necessary debt destruction.

I've long contended that, much like the Internet prophecy proved true -- but not before the tech crash -- so too would globalization, albeit not without painful-yet-necessary debt destruction.

To get through this, we need to go through this. If we're not allowed to go through it, foreigners will seek alternative avenues. Remember, for holders of dollar-denominated assets, seeds of discontent have been sowing under the surface for years, with the greenback off 30% since 2002.

More likely than not, global leaders will watch how our new administration attempts to tackle the financial crisis before taking drastic steps. They understand that co-dependent risk exists as a function of the derivatives that interweave our financial infrastructure. If they could disassociate from our economic ecosystem without inflicting massive damage on themselves, they would have done so long ago.

If forward policy attempts to induce more debt rather than allowing savings and obligations to align, we must respect the potential for a system shock. We may need to let a two-tier currency gain traction if the dollar meaningfully debases from current levels.

If this dynamic plays out -- and I've got no insight that it will -- the global balance of powers would fragment into four primary regions: North America, Europe, Asia and the Middle East. In such a scenario, ramifications would manifest through social unrest and geopolitical conflict.

This particular path isn't something one would wish for, but the cumulative imbalances that steadily built in our finance-based economy must be resolved one way or another. Therein lies the critical crossroads we together face as our wary world attempts to find its way.

Scary? Yes. Probable? Not so much, at least for the time being. Possible? Certainly, although I'll again offer that it could take years before the pieces of this prickly puzzle fall into place.

Effective money management dictates weighing the entire probability spectrum of potential outcomes and factoring them into our decision making process. While the notion of a seismic currency shift may seem obscure, we must respect the possibility long before it becomes front-page news.

For if we've learned anything through the last few years, proactive thought provocation is a necessary precursor to effective preparedness.