(Image) http://www.nowandfutures.com/images/economic_cycle.png

{kind=link}

Sunday, March 30, 2008

Economic Cycles and Political Trends in the United States (Part I)

"The issue today is the same as it has been throughout all history, whether man shall be allowed to govern himself or be ruled by a small elite."

Thomas Jefferson (1743-1826), 3rd U.S. President

"I have learned to hold popular opinion of no value. "

Alexander Hamilton (1755-1804)

"Those who cannot remember the past are condemned to repeating it."

George Santayana (1863-1952)

[N.B.: This article is drawn from a conference to be pronounced by Dr. Tremblay before the Florida Renaissance Academy, Marco Island Yacht Club, on April 4, 2008. Those wishing to attend can call: 239-394-3089 or 239-434-4737]

PART I

I have been a student of cycles, both of economic cycles and of political trends, for a very long time. To try to understand the economy or politics for that matter without having a knowledge of cycles and trends is like sailing without a compass, a weather report or a GPS (Global Positioning System).

There are four main types of cycles in economics, some relatively short, such as the slightly less than four year long inventory cycle, or the standard 10-year technology cycle, and some longer, such as the 18-year long real estate cycle (N.B.: We are presently in the downward part of this cycle, which should last until 2010-11), and some called long waves, such as the 54- to 60-year long Kondratieff cycle of a debt and price inflation-then disinflation-followed by a debt and price deflation (N.B.: We are presently in the deflation phase of this long cycle, a good example being the debt deflation of heavily levered banks and hedged funds and of price deflation in housing) such a deflation phase expecting to last also until 2010-11.

As I mentioned, the shorter cycle is the inventory cycle (Kitchin), which lasts slightly less than four years. This cycle has become very much less pronounced in recent years for two reasons. 1) First, the service sector as a percentage of the entire economy is much larger than it was 100 or even 50 years ago. In the United States, the service sector accounts for approximately three quarters of GDP. Today, four out of every five private sector non-farm jobs (80 percent) are in the economy's service sector (federal, state and local government, wholesale trade, retail trade, transportation, public utilities, construction, finance, insurance, real estate, telecommunications, computer and related services, energy services, distribution, express delivery and audio-visual services, etc.). —50 years ago, the service sector accounted for about 60 percent of U.S. output and employment. Today, the information age has generated new forces that have driven the shift to a more services-oriented economy.

For the U.S., services exports represent approximately 30 percent of the total value of America’s exports, and it is in surplus. This sector of the economy is much less volatile than manufacturing, agriculture or mining.

2) Second, over the years, businesses have embraced the use of the computer and the digital revolution to manage inventories. This has lead to the "Just-in-time" inventory management method, which has considerably reduced fluctuations in the inventory stocks of distributors, thus smoothing the production cycle of producers.

During the entire twentieth century, as the economy moved from agriculture and industry and more and more toward service industries, the volatility of the US economy became less and less pronounced. As a consequence, recessions have been shallower and of shorter duration. And, of course, there has not been another economic depression, like the 10-year Great Depression that lasted from 1929 to 1939.

—There was another structural development on the inflation side. Indeed, the internationalization of national economies has acted as a damper on price increases, as new low cost producers, such as China and other emerging economies, have entered the markets. For instance, exports and imports used to represent 20 percent of the U. S. economy; nowadays, it is 30 percent.

Sometimes we measure these cycles from bottom to bottom, and sometimes from top to top. For the 10-year cycle (the Juglar cycle), it often coincides with normal recurring recessions. In the U.S., there were recessions, for example, in 1969, in 1973-75, in 1980 and 1981-82, in 1990-91 and in 2001, most of them within about a 9-10 year interval. According to this cycle, there could be a somewhat severe recession in 2010-11, possibly following the slowdown or recession expected to occur this year.

What is of interest is that the real estate cycle or housing cycle (the Kuznets cycle) is also scheduled to bottom in this period. This is a cycle of about 12 years of price increase and of 5 or 6 years of price decline. The previous cycle, from top to top went from 1987 to the spring of 2005. A bottom would therefore be normal in 2010-11 and a future top around 2023.

But the multi-generation Kondratieff cycle is perhaps even more ominous in its influence on the economy. From bottom to bottom, this very long cycle began in 1949, when wartime prices were unfrozen, reached a top in inflation in 1980 at 13-14 percent levels, and is expected to bottom between 2003 and 2010. The current financial crisis and the credit crunch that accompanies it are the main players in this long cycle.

As you see, the table is set for an important economic bottom in the next two years. That is why I recommend being careful and alert financially during this turbulent period.

There are also cycles and trends in politics, and they sometimes coincide with economic cycles. For example, it would surprise no one to know that during the early inflationary phase of the Kondratieff cycle, a philosophy of government social spending would tend to prevail. In the U.S., this would be a period where the Democrats would be expected to be in power. When there is a need to fight inflation, a conservative philosophy of government would tend to prevail, and this would favor the Republicans. The Kennedy-Johnson administration of the 1960s is a case in point, while the Reagan-Bush Sr. administration is the other.

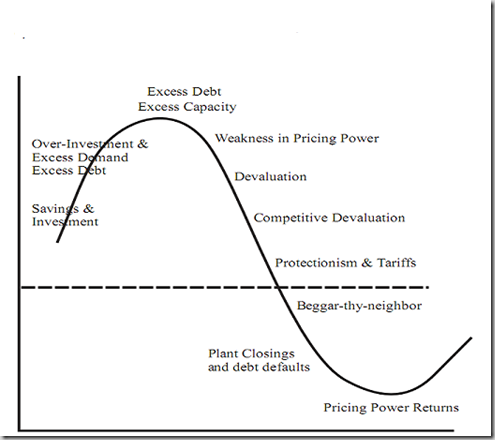

See graph Economic Cycles.

(To be continued next week)